Cryptocurrencies, love them or hate them, are doing better now than ever before and have recently hit a total market value of over $1 Trillion…..yep, $1,000,000,000,000. But what does that mean to the legal world? Artificial Lawyer talked to David Fisher, Founder of Integra Ledger, the legal blockchain system, about the implications. We started with money and ended up on democracy.

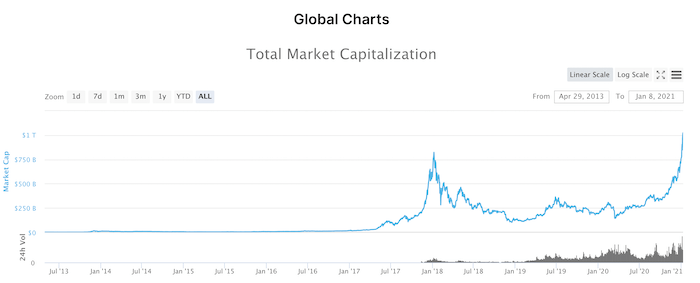

First the money. CoinMarketCap data shows that as of today the total value of all the many hundreds of cryptocurrencies in the world (i.e. digitally-based currencies) is now $1.023 Trillion. Although, of this almost 70% is Bitcoin, the token that started it all.

However one looks at this the figures speak for themselves – thousands of people around the world have sunk their money…..fiat money, i.e. pounds and dollars, into assets created out of ones and zeros. And, you can spend crypto more easily now than ever before. There are credit cards that link to your crypto account and there’s a growing list of companies that accept these currencies. Even well-known charity Save The Children now accepts Bitcoin donations.

OK, so they are getting more accepted, increasing in value and working their way more and more into the economy. This helps to generate work for lawyers on a variety of fronts, from advising the crypto companies to more broadly helping with commercial law matters that relate to this particular type of asset. E.g. if a person leaves a Will in which crypto assets are listed, how are these handled? Or, what about contracts between parties that have a crypto element? And then there’s all the regulatory work and inevitable disputes involved in launching and selling crypto. So, there’s that.

But, is that all? Is this just generating some additional work for lawyers without really changing anything? Now to Fisher, who is very optimistic about the long-term role of crypto and blockchain technology.

‘As always, Bitcoin is proving the merits of blockchain – specifically, that distributed trust is very formidable compared to social trust in centralised authorities,’ he explains.

OK. But, how did we get from money to social trust in governments?

‘Bitcoin has a hard cap of 21 million Bitcoins that will ever be created, and no single party can arbitrarily change that. By contrast, central governments are printing money at an astonishing rate, steadily debasing the value of currencies held by populations,’ he continues.

But, how does this impact the legal world? Fisher adds: ‘The implications for the legal industry are indirect but substantial. Like all blockchains, Bitcoin is a data trust network (Bitcoins aren’t actual coins – they are numbers).

‘As this technology is applied to more and more data in the world’s economy, it will change the way that organisations move information among themselves, including documents, contracts, invoices, and data in general.

‘It will be akin to the technological leap from travel by train to travel by airplane. The former was slow, expensive, inefficient, and constrained by the enabling infrastructure (the tracks), and the latter is fast, efficient, and flexible (fly virtually any route).’

I.e. crypto values are simply a reflection of the growing importance and acceptance of a blockchain approach to data. One could call it an indicator of what is going on at a deeper, systemic level.

But, one aspect that really intrigues Artificial Lawyer is the focus on moving away from centralised authorities, e.g. the Bank of England, the US Treasury, the European Central Bank.

This site asked what is so wrong about centralised authority, not just in relation to controlling and producing currencies, but in general? And that’s a question that leads to some deep questions about democracy.

For example, maybe centralised authorities are actually a very positive thing, but as a society we need to be better at holding them to account and having oversight of their actions? One could argue that if you can improve how centralised authority works then there’s no need for this massive experiment in decentralisation. I.e. can you not just make the system we have work better, rather than throw the whole thing out or create a parallel system operating with a different approach?

Artificial Lawyer put this to Fisher. He replied: ‘The public blockchains specifically undermine centralised authority and control of information and value.’

‘Where I come down on things is that, whether from the left or right, power, control, and wealth is centralising, and that’s generally a bad thing.

‘Anger from left and right is similar, arising from a feeling of loss of power and agency in life. The financialization of the economy has shifted huge rewards to the financiers, and technology has shifted vast control and wealth to the technology companies. Neither are democratic. They are radically, intensely self-interested.

‘Government, finance, and technology are arguably in bed with each other. On balance more power at the personal level is better, and that argues for decentralization in an orderly way.’

So, there you go. And perhaps this helps to explain why people who are interested in blockchain and crypto are so passionate about it. For Fisher, and many others, this is not about a currency value on a chart somewhere, or just how data is moved around or accounted for, it’s about a whole new approach to how society works.

Any road, as mentioned at the top of the story, whatever your view of blockchain tech and crypto, they are not going away, and if current evidence is anything to go by, this approach is steadily working its way more and more into our lives.

The big question is whether this will remain in effect a parallel economy, or whether the mainstream centralised economy will move in blockchain’s direction and join it? And that’s a question several central banks have already explored, with China perhaps taking the most radical steps in terms of creating their own digital Yuan – but more on that another time.

—

Plus Aaron Wright, a Professor at Cardozo Law School in New York, and Co-Founder of smart contract pioneer, OpenLaw, added: ‘Bitcoin and Ethereum’s breakouts this year appear to be driven by institutional adoption. Digital assets are going mainstream.

‘What does that mean for legal tech? It should open up more opportunities for programmable assets, using smart contracts. Today, lawyers program how assets and value move in commercial settings using traditional natural language contracts. Over the next decade, that could be increasingly replaced by software.’

Wright, who through OpenLaw also launched the LAO project – a ‘legal distributed autonomous organisation’ aimed at investing in Ethereum-based ventures – added: ‘The growth of Bitcoin and Ethereum could also be accelerated due to general technology trends.

‘We’ve seen Covid push the adoption of digital technology across industries. That revolution is not going to be limited to Zoom and video chat platforms. Eventually (and the big question is when) digital tech will replace and change how the legal industry is structured.’

Discover more from Artificial Lawyer

Subscribe to get the latest posts sent to your email.