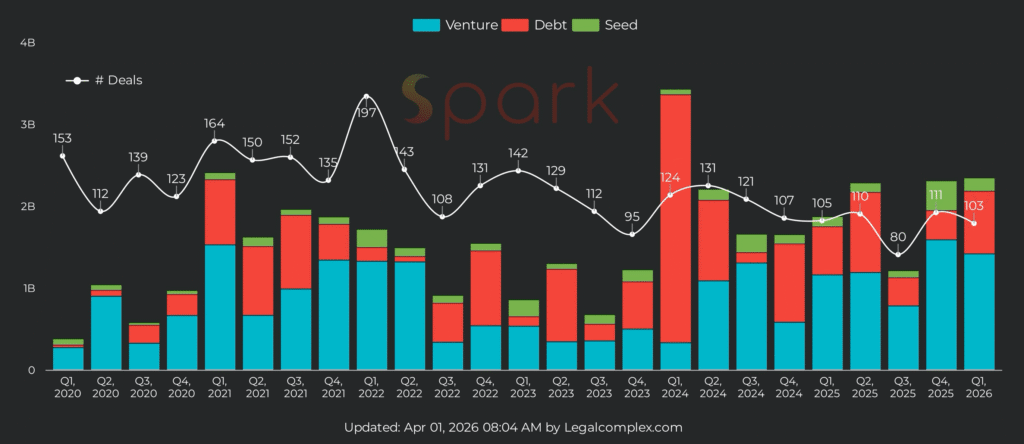

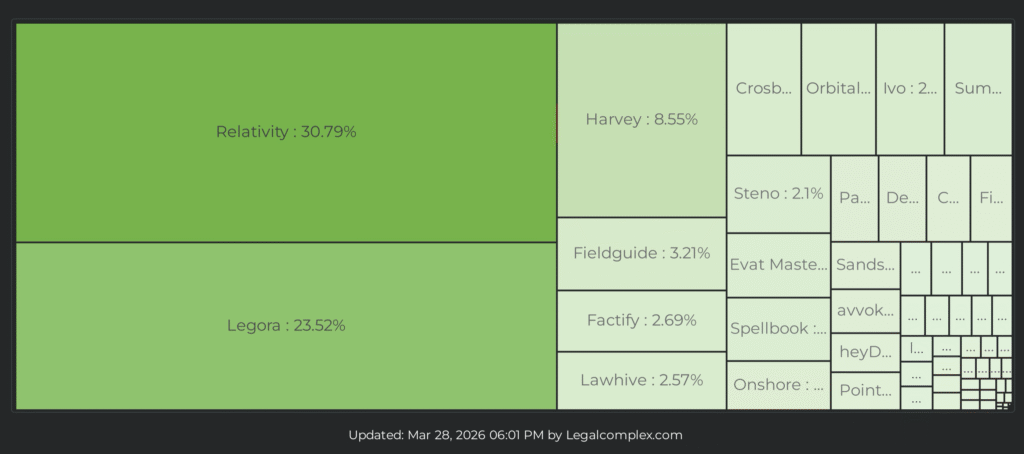

Legal tech funding continues to remain strong, with Q1 2026 data from Legal Complex showing that $2.34 billion was raised across 103 deals. However, Relativity, Harvey, and Legora represented around 63%, or almost two-thirds of the total, in a mix of equity and debt.

That said, Legal Complex found that based on its sample, the median round was just $1m. So, this is a top-heavy scenario, with several companies scooping up most of the money, but there is also a very long tail, with dozens of companies raising still – but, far more modest sums.

For once it was not Harvey or Legora that changed the picture most of all this Quarter; it was Relativity’s $720m debt facility announced in January, representing 30.79% of all Q1 funding by itself. And as readers will remember this comes ahead of a potential (and it should be underlined….potential) IPO.

Meanwhile, Legora raised $550 million in a Series D round out of Stockholm on March 10, bringing their cumulative total to $816 million. Harvey added another $200 million Series G round on March 25, pushing their lifetime raised to $1.22 billion, Legal Complex said.

For context, ‘Harvey has now raised over a billion dollars in roughly three years of existence’ – and no other legal tech company has ever done this with VC funding…aside from Clio. Plus, we are far from the peak of these rounds for the Hargora duo. There is much more to come.

Other notable rounds, according to Legal Complex, included:

- Fieldguide raised $75 million (GRC, San Francisco),

- Factify pulled in a $73 million seed round (Documents, Tel Aviv),

- Lawhive raised $60 million (Legal Services, London),

- Crosby closed $60 million on the last day of the quarter (Contracts, New York).

- Orbital Witness ($60 million, London),

- Ivo ($55 million, San Francisco),

- Summize ($50 million, Manchester) rounded out the top 10.

If you look at these …. (who is Fieldguide..?) then they represent a range of needs, although several have a strong contract focus. Interstingly, both Crosby and Lawhive are ‘NewMods’, although using different approaches. Meanwhile, Orbital – see following story – is about to launch its own law firm as well.

In short, AL noticed with interest that three of the top ten raisers are related to new approaches to offering legal services. And that is a sign of the times as well!

Raymond Blyd, founder of Legal Complex, commented: ‘My favourite stat to watch each quarter is the ratio of late versus early stage fundraising.

‘In Q1 2026, seed deals (46) overtook growth deals (44) for the first time since Q1 2024. The crossover first happened in Q4 2023 when seed hit 66 against growth’s 58, then became pronounced in Q1 2024 (seed 81, growth 50).

‘After briefly reverting through 2025, seed is back on top. That suggests a fresh wave of legal AI startups entering the market. The question is whether they’ll find their way to Series A or join the growing pool of companies that raised seed between 2023 and 2025 and haven’t raised since. That number was 979 when I last checked.’

Thanks to Raymond as always for the data.

AL Comments

A couple of additional points AL would make are:

- How will Claude for Word change valuations of some of the smaller, narrower document-focused startups? It’s not a slam dunk that lawyers, at firms, or inhouse, will shift over to Claude for doc review. But, it may well play on the minds of investors who had previously assumed that their contract AI portfolio company was onto a guaranteed growth trajectory.

- Will there be consolidation? For years and years the wider market has been talking about a possible consolidation of legal tech companies, on the basis that in any rational economic environment you cannot have dozens of startups all offering overlapping products. However, time has shown that the legal market can indeed support such a scenario. Why? Because it’s huge, complex, atomized, and law firms tend to like to make their own choices as to what products to buy.

- Last point, as seen above, Hargora have now raised so much money and have such significant GTM capabilities, it’s hard not see them growing and growing, which in turn will draw in more investment, and on and on. The question is: will this impact the other companies? We can already see the vast difference in funding rounds. And yet, as noted above, the legal market seems happy to sustain dozens of companies when perhaps other verticals might focus on just a handful of market leaders. In which case, we are well on the way to a market dominated by what AL is seeing as the Big Five legal AI platforms: TR, Lexis, Harvey, Legora and Clio, with a group of close followers of smaller size also seeking to offer broad platforms, and then dozens and dozens of other companies operating across many different segments of the legal tech market.

- To conclude: yes, huge amounts of money are coming into legal tech and yes, new formations are starting to take shape, but overall the general character of a highly atomized legal tech market, with likewise dozens of investors supporting a myriad of products remains very much true still.

More at Legal Complex – which is now back to full force – here.

—

Legal Innovators – California and Paris – June

You can now do express registration to join Legal Innovators California and Legal Innovators Europe in Paris this June.

A Legal Tech Conference For All of Europe

Legal Innovators Europe – Paris – June 24 and 25.

Express route to your ticket here.

And,

Express route to your Legal Innovators California June 10th and 11th ticket here.

Legal Innovators California, the landmark West Coast legal tech event, will take place on June 10 and 11, in the heart of the Bay Area, the home to many of the world’s leading AI businesses – and plenty of legal tech pioneers as well! More information and tickets here.

Discover more from Artificial Lawyer

Subscribe to get the latest posts sent to your email.