Onit had just bought spend management system Bodhala when CEO, Eric Elfman, spoke to Artificial Lawyer. He was upbeat, noting that Onit would now do ‘two to three acquisitions’ per year. However, he believed that ‘you can’t build a $1bn revenue [tech] company on legal alone’ and that Onit would eventually start to buy up companies in other sectors to attain the scale it wanted.

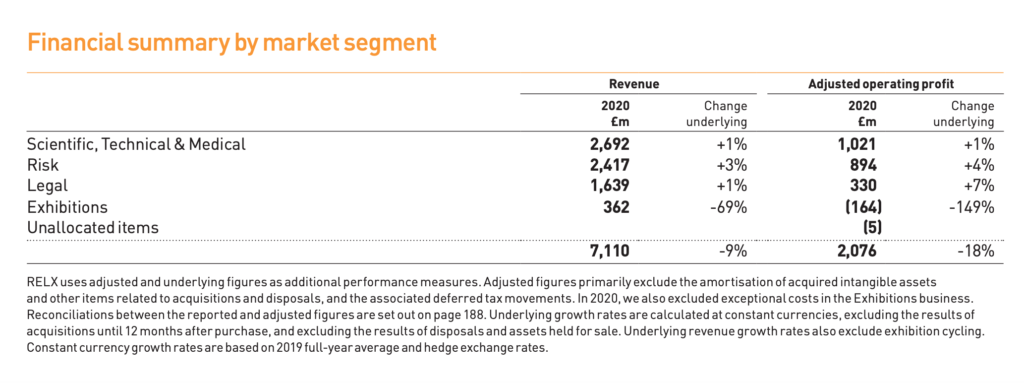

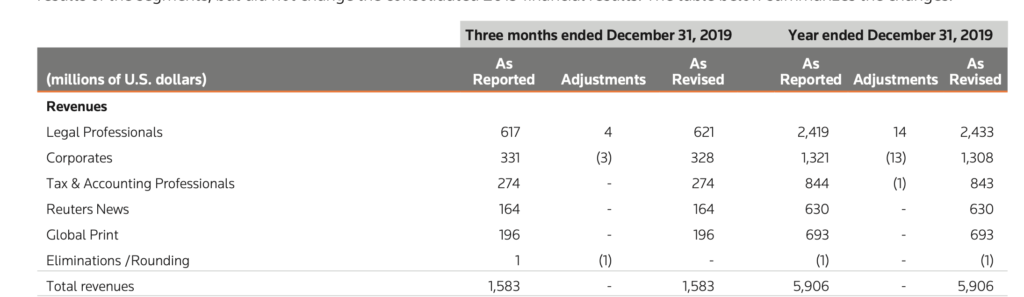

This is significant on several levels. First, there are of course at least two legal tech companies with revenues over $1bn – Thomson Reuters’ legal arm made around $2.4bn in 2019, and LexisNexis (i.e. the legal division of RELX), about $1.6bn in 2020, (see tables below).

And,

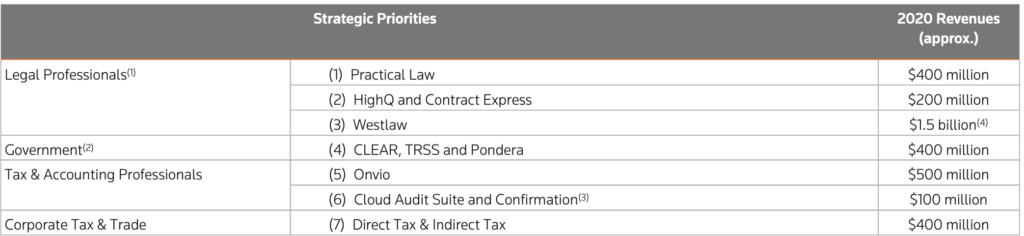

But – and this is the key point here – legal research, based on the two companies’ massive case law libraries – made up the bulk of this income. In Thomson Reuters’ case, Westlaw had a revenue target in 2020 of $1.5bn, with Practical Law – in effect another legal data library of sorts – aiming for $400m in revenues. In comparison two of the key tech offerings that are not primarily about access to legal data controlled by Thomson Reuters, e.g. HighQ and Contract Express, were aiming for $200m in combined revenues globally.

And, if we look at other very large companies, let’s take Relativity for example, one of the biggest brands in eDiscovery software, their revenues are estimated to be around $100m.

In short, if we put the giant legal data depositories to one side – and there are only two of these at this scale (as vLex and Bloomberg Law are estimated by this site to have notably lower revenues) – then Onit’s Elfman is absolutely right. Hitting over a $1billion in income per annum from selling just software to law firms and inhouse legal teams is very, very hard to achieve.

One reason why Westlaw and LexisNexis have succeeded here is because: 1) they started out very early in their quests to build the largest legal data libraries on the planet, which then became digital libraries that are now searchable with the latest NLP technology, and 2) the number of lawyers that want access to some kind of case law library is in the millions on a global basis – and with those kinds of numbers you can generate a lot of revenue.

But, selling CLM software, or an NLP doc analysis tool, in a market with multiple players, and sometimes relatively small differences in many cases between product offerings, is a different thing entirely.

Moreover, although it can sound like the legal market is massive, the number of law firms that want to buy automation technology, for example, is not quite so big. We are really looking at a number in the 100s, rather than the 1000s of firms, which consume most legal tech on a worldwide basis. The same could be said of large inhouse legal teams.

There is, as yet, no legal tech company with a Salesforce ubiquity. And, as a benchmark, Salesforce has revenues per year of around $21bn – or almost nine times what Thomson Reuters’ multi-decade effort to take marketshare in the legal world has achieved.

So, what next? Elfman told Artificial Lawyer that for now they will double down on legal and focus there. After taking $200m in investment from K1 Investment Management in 2019, they have already made several deals.

Bodhala is its fourth recent M&A deal. In November 2020, Onit acquired legal AI company McCarthyFinch and then document automation leader AXDRAFT 30 days later. Onit also acquired SimpleLegal, a ‘legal operations software provider’, in May 2019.

But, back to the key point. Once Onit has built out its enterprise legal management platform, which includes CLM and around 200 bespoke workflow solutions for corporates, what then?

Elfman said that they may then need ‘to replicate this in another vertical such as HR, sales, or finance’.

‘You will see us do M&A in a sector that is a totally different vertical,’ he underlined.

And this makes a lot of sense, as the company states on its website: ‘Onit partners with businesses to build custom enterprise-wide software solutions that can be implemented quickly, are easy to use, and drive better decisions.’

If you are partnering with businesses to build enterprise solutions then why not move into other verticals? Also, as is often explored by this site, as more tech companies engage with the inhouse world, the more the idea of contract-related data as needing a company-wide approach develops, as keeping all this value in the legal team creates too much of a silo.

Add that to the ability to create workflows across other business functions and you have some interesting synergies. With K1 behind it, the company, which got started in 2011 and now has around 600 corporate clients, could grow significantly.

But back to the beginning. What does it mean if very, very few legal tech companies will ever hit $1bn in revenues?

First, it does put something of a ceiling on the recent IPO hype. Although a company might have a massive valuation, the reality is that real world revenue doesn’t lie, and beyond that, actual profit is even more of a financial truth. Buyers into listed legal tech stocks may assume that all those going to market now will become the next Salesforce, but with a legal focus – yet, according to Elfman they’d likely be wrong to assume that.

As this site explored after the Litera/Kira Systems deal – (Could there be just one legal tech platform), creating an ‘ultimate platform’ is really hard to do – and as noted then, it is the inability to have what Westlaw and LexisNexis have in the shape of their massive legal data libraries that makes it so hard.

Another aspect is the money involved in trying to get that big in a short time. K1 has invested $200m in Onit. But, a half-dozen more M&A deals could absorb that in a couple of years, depending on the size of the targets. And that’s another aspect, sale prices naturally are higher than the revenues of the targets, as you are making an investment in the future growth of the acquisition. Inorganic growth capital eventually runs out and then you have to depend on organic growth – or merge with a compatible company. But, merging two CLM companies together may not be easy to do, unless their products were very similar.

And, one other path is to do an IPO, as others have done. On that score, Elfman is sceptical of the current valuations for legal tech companies and was far from excited about taking the same path, so it doesn’t look like Onit will go the IPO route any time soon.

Conclusion

While the last year or so have been marked by a sense that there is no ceiling to the growth of legal tech, Onit’s message is that although there is plenty of growth opportunity in the market, especially via using an M&A strategy to build a much larger platform, we shouldn’t expect to see a raft of $1bn revenue legal tech companies emerging, regardless of the sometimes wild IPO valuations.

To go beyond that billion dollar barrier, legal tech companies will have to look at new sectors, becoming more multi-purpose enterprise companies that serve far more than lawyers. And some ‘legal tech’ companies are indeed taking that strategy already. For example, both BRYTER and Eigen Technologies see themselves as multi-sector companies, with legal as just one part of the client mix.

Ultimately this means that although legal tech is growing now like never before, we should not assume that this sector can easily replicate what we see in other parts of the business world.

Discover more from Artificial Lawyer

Subscribe to get the latest posts sent to your email.

1 Trackback / Pingback

Comments are closed.