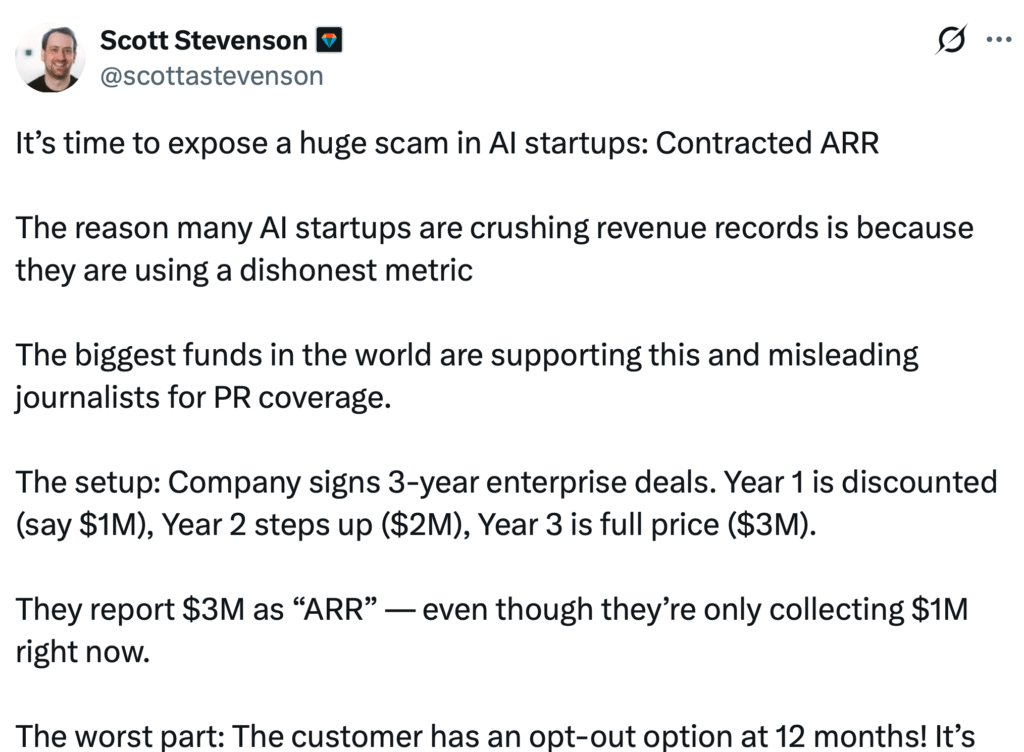

Legal tech companies, and especially VC-fuelled startups, have an ARR problem. At its core is how you define ‘Annual Recurring Revenue’. Things have come to a head and Scott Stevenson, CEO of Spellbook, has suggested ‘a huge scam’ is happening (see below). Meanwhile, Artificial Lawyer would say that because ARR is such an unclear metric, startups may be quite unintentionally causing confusion.

Those startup founders and legal tech experts who Artificial Lawyer contacted this weekend agreed that ARR is easily prone to abuse, and at the very least it is open to misunderstanding from the market in general.

Central to the problem are two key issues:

First, that ‘ARR’ can potentially include contracted future income that you are not receiving yet – if that’s how you want to interpret it. And some refuse to do that, while others do.

The issue here is that your company may have just agreed to a $0 deal with a law firm in order to low-ball the competition and win the customer. Within that deal is a promise – which of course can be cancelled by the law firm – for them to pay $1m for the software at some point in the future, e.g. in year 2 or 3.

But, if you say that’s ‘ARR’, many people simply read that as real ‘revenue’, i.e. ABC legal AI company has made $50m this year. When in reality it is making $25m.

Plus, because future income is not guaranteed, then they really cannot say that anything will be ‘recurring’. Law firms can break those deals. They can pick new vendors. Anything can happen over three years.

The second problem – and AL was surprised to find this out – is that ARR does not have a formally agreed upon definition.

If there is no definition, then a startup and its VC backers can make it mean what they want to. But, the most important outcome here is that many people assume that the big $$$ number attached to the ARR press release is actually ‘real revenue’ – and it may not be the case at all.

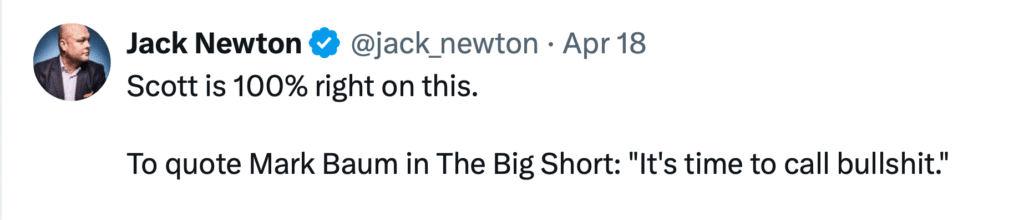

In fact, Jack Newton, CEO of Clio, added in a tweet referring to Stevenson’s post on X that ‘It’s time to call bullsh*t’, on the confusing use of ARR.

–

Who Gains? Who Loses?

Why does this matter? Well, it matters a lot for multiple reasons. Here’s some thoughts on who it helps and who it harms.

- Law firms and inhouse teams like to pick legal tech companies they believe are going to last. So, very strong revenue numbers send a confident message that you will be staying in the market. But, are they getting the wrong impression?

- Potential hires may join a company that looks like it’s got great revenues, not just because that gives reassurance, but also because of the opportunity to gain stock options. If they knew the real data, would they be so attracted?

- Other investors who are looking at a target should, of course, know better than to trust unexplained ARR numbers. And in fact, some third-party research AL saw this weekend suggests that some VCs don’t even believe ARR numbers they see published by startups. One legal tech company AL spoke to said that they are aware of the potential for discrepancy and maintain ARR and Contracted ARR or cARR numbers at the same time. I.e. future money they have a contract for and money they are really getting right now. In their case, they said the difference between the two was below 5%. Yet, in other companies, how big is that gap? The answer is: we have no idea.

- And more broadly, having a blurred and unreliable metric such as ARR used widely in legal tech undermines the market. If people start to doubt what legal tech companies say in public, then it harms the whole sector.

ARR’s Definition Problem

In the early – and much calmer – days of legal AI, startups just talked about revenue, i.e. literally referring to how much money they had made that year, based on real customers who had actually paid them real money that was now in the bank.

But, fast-growing legal tech startups these days, running on VC rocket fuel, prefer ARR – a term that was developed for a new breed of SaaS companies that planned to grow massively month on month via subscription. In fact, its roots really go back to what is called ‘run rate’, or the monthly revenue, and then 12X-ing it to give you an annualised figure – even if that was largely fictional in some cases.

I.e. ARR is based on the assumption that a company is growing so fast that a normal revenue figure is impossible, as the VC cash is helping them to acquire new customers so quickly. But, the flipside is that we then end up with the problems above.

A Solution?

Is there a solution to this? One way forward is for all companies to be transparent about cARR vs ARR. I.e. say to people: ‘We have contracts that might theoretically in the future yield this level of income, but right now the actual real money we have coming in is another number, which in April this year is X.’

That way we can at least have some idea of what’s real and what is projected.

Another way would be to get together and for legal tech companies to agree on how we use ARR: to create a standard definition and then for everyone to stick to it.

It’s doable. Legal tech founders just need to agree to the convention.

Or, we all start to use another figure, maybe a new one entirely? But, that would depend on the VCs accepting it, and that seems unlikely as many of them are wedded to the whole ‘rocket fuel’ in, accelerating ARR out methodology, as that plays well for them. After all, VC funds want to see growing investments and those who contribute cash to them – the LPs – also want to see the investments going well.

Conclusion

Whatever the way forward, we need more clarity. We cannot allow the use of a blurry metric to harm legal tech as an industry.

The way to address that is a clear definition and openness among all participants, from VCs to startups.

The irony of all this is that the startups which are now broadcasting their ARR numbers are all doing amazingly well. Even if they used the most conservative definition possible of how much they are earning it would still be impressive. There really is no need to allow the market to get the wrong idea, even if this happens unintentionally.

—

Call for views: Artificial Lawyer has spoken to several people over the weekend. In each case it was all off record. This site would like to do a follow up piece containing your on the record views. If you’d like to send in how your company handles ARR, what definition you prefer, and any other comments on the market, then please email me. Or feel free to make a more public comment connected to this article on socials. Thanks.

Richard Tromans, Founder, Artificial Lawyer, April 20, 2026.

—

And here is a link to Scott Stevenson’s full tweet – here.

Discover more from Artificial Lawyer

Subscribe to get the latest posts sent to your email.