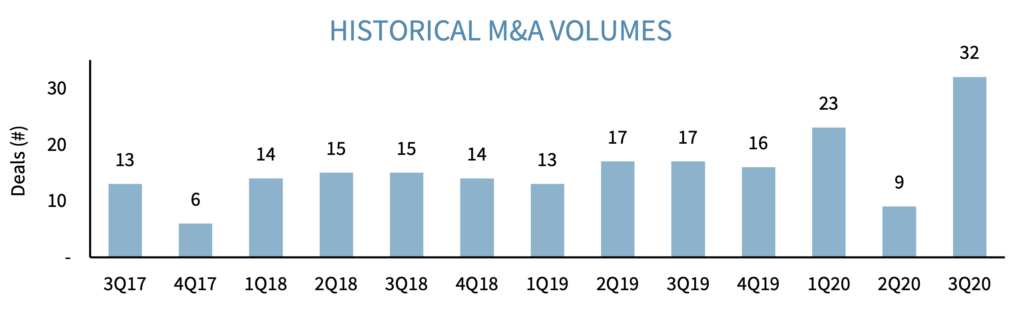

A new report on investments and M&A in the legal tech sector by advisory business Raymond James has shown there is a significant boom in acquisition activity, largely driven by private equity (PE) funds. In Q3 2020 there were 32 M&A deals involving legal tech companies – compared to an historic average of around 15 per quarter.

Interestingly, the targets are not the newest and flashiest of tech solutions. As report co-author Junya Iwamoto commented to Artificial Lawyer: ‘This is about ‘Legal Tech 1.0’. It’s still mostly the mature companies, with buyers looking for traditional M&A synergies such as cost savings and new market entry. This has mostly not been about bleeding edge, new legal tech companies, i.e. Legal Tech 2.0.’

As seen below in Table 1, Q2 2020 saw a dip in deals, likely caused by the onset of the pandemic. But then, with 32 deals in Q3, there was a surge that was around double the usual level of activity. Part of this could be because of held back deals now coming to fruition, but even taking that into account Q3 has experienced a peak unlike anything seen before.

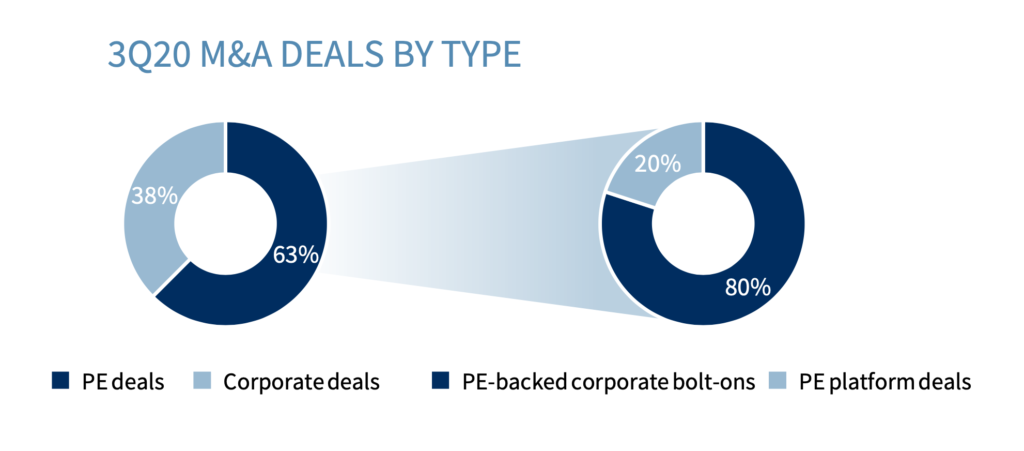

Of additional importance are the players that are driving these deals, which as seen in Table 2, are very often PE funds.

As seen above, 63%, or a little under 2/3rds of deals were driven by PE funds. Of these the majority were ‘PE-backed corporate bolt-ons’, i.e. a company that is owned by one or more PE funds buying up legal tech companies to add to what they already have.

What this tells us is that the overall strategic play here is building out larger, multi-capability brands. Building large-scale legal tech brands should in theory make them more capable of taking market share as they will more easily be able to compete with the likes of LexisNexis and Thomson Reuters, and other large well-established companies.

Also, from a PE fund’s perspective, they will get better returns when they sell by building one very large platform than sinking time and effort into a number of small deals where the targets cannot combine into a larger offering.

Some of the deals are shown below:

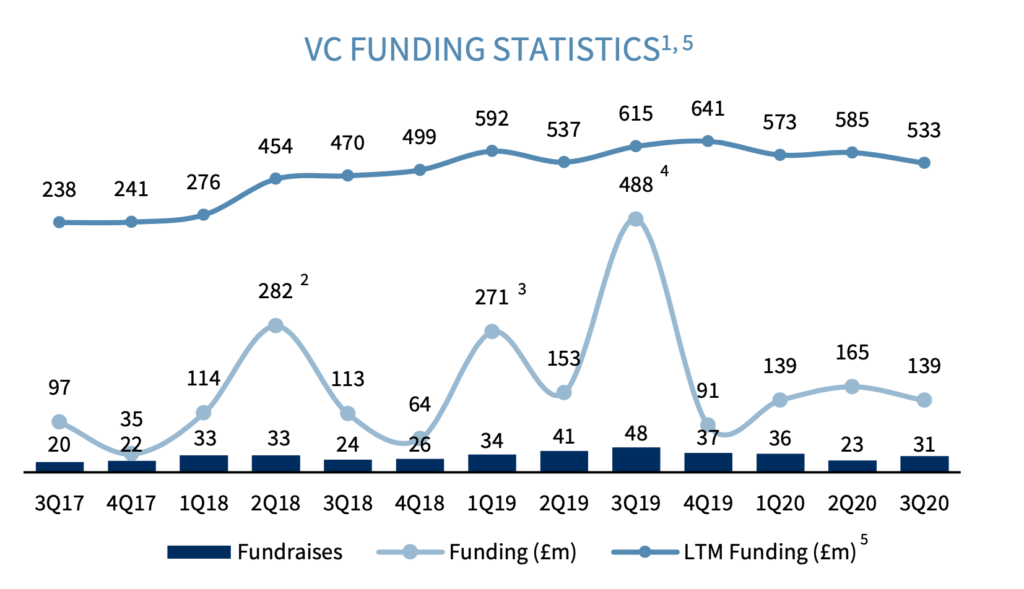

On the VC and PE investment side, things have been less strong than last year (see Table 4).

Q3 2020 was worse than Q2, with £139m raised in growth capital. What is really different is how things compare to 2019 – which saw a surge in investment and in Q3 2019 saw £488m in funding. But over the longer term, so far 2020 has not been terrible for funding if one compares it to the first three quarters of 2017, for example.

One could say that the current funding levels – amid a pandemic – are not as bad as many had feared. Proof of that has been seen in the number of stories in Artificial Lawyer about scale-ups gaining funding.

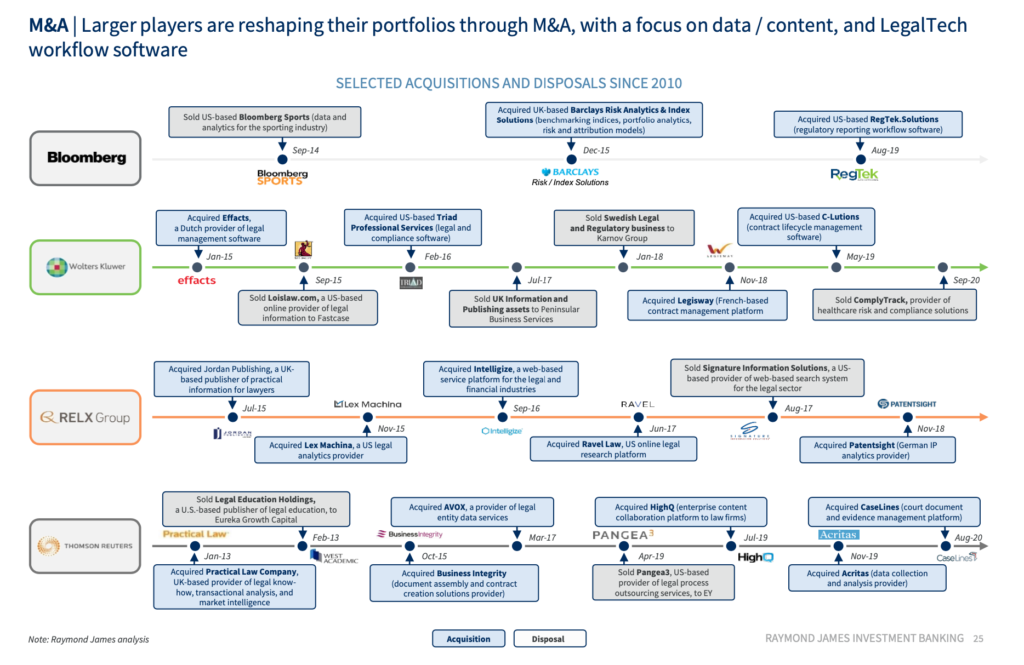

One other interesting part of the story is how the large legal tech companies, such as Thomson Reuters and others, have been reshaping their collection of legal tech/NewLaw capabilities through both purchases and sales.

As seen in Table 5, the impact of Bloomberg, Wolters Kluwer, LexisNexis and Thomson Reuters on the shape of the market cannot be overlooked.

Overall, the conclusion is that we are seeing more consolidation with more and larger platforms being created – this is driven by PE funds with a lot of cash and the goal of building globally significant legal tech companies.

Investment is ‘ticking over’ one could say and is doing better than one might expect. This suggests that once the pandemic passes there will be even more VC activity, as if it can be like this in a downturn, then in a good year it should really bounce upwards.

Discover more from Artificial Lawyer

Subscribe to get the latest posts sent to your email.

1 Trackback / Pingback

Comments are closed.